Problem & Approach.

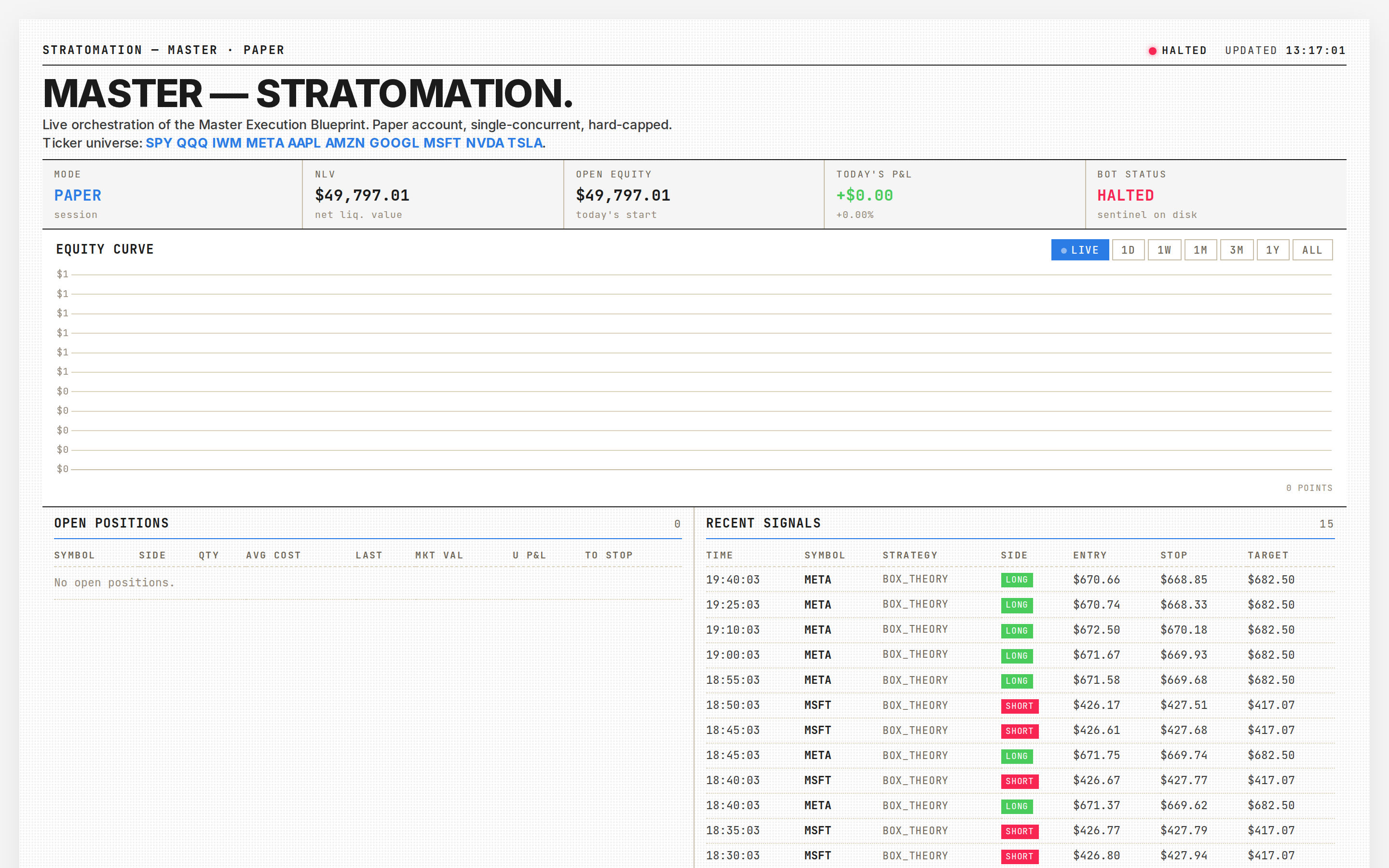

Box Theory is one of seven strategies in the Stratomation blueprint — SHORT on PDH rejection, LONG on PDL reaction, both inside a defined day-range box. I wanted it executed by a bot, observable via a public dashboard, with paper-only safety. Stack: Python 3.12 + ib_async + IB Gateway (Docker container with IBC auto-login) + FastAPI + APScheduler + SQLite + PM2. Cron schedule: 09:20 pre-open, 09:45 trader activate, every 5 min poll, 15:55 auto-flat, 16:30 EOD. Layered risk: per-position 2.5% stop, daily loss cap 2%, max concurrent 5, max position 15%, HALT sentinel file. The first per-position stop fired exactly at 2.51% loss on day 3 — capped damage at ~$34 vs the 3-5% it would have ridden to auto-flat.

Outcome.

Phase 3 complete on day 3 (2026-04-27). Day 3 P&L: -0.31% NLV — bounded loss on a one-sided bullish day where range-reversion fights the trend. The public read-only dashboard lives at stratomation.reblis.com. Phase 4 (more strategies) and Phase 5 (live flip) are gated on a bracket-ghost-orders blocker documented in FOLLOWUPS.md.